Treasurer Morrison delivered the Federal Government’s 2018/2018 Budget on Tuesday night. We share our thoughts on the key issues that impact you.

We get it

We understand that not everyone gets excited about Budget night the way we do. We get it, we truly do.

We get excited because there is a chance each year that the Treasurer each year will make announcements that result in material changes to the way we advise our clients. Typical changes relate to superannuation laws, tax rates and changes to finance rules. We monitor these changes and decipher what they mean for you each year. In some years we see material changes, in other years we do not. 2018 saw few changes that impact you in a material way, in our opinion. Some changes result in slight changes and most of them are positive. It is safe to say this is a ‘pre-election Budget’ (when people say that, they really mean the Budget doesn’t offend many people and most of the changes are positive with little pain doled out).

The speech

Treasurer Morrison’s 4326 word speech was delivered in the customary 30 minute slot between 7:30pm and 8:00pm.

Below we have created a word cloud of the main words he used in his speech to give you a visual representation of the concepts he was trying to get across.

Some key figures from the Budget include:

- A relatively small $2.2 billion surplus is forecast for 2019-20, one year ahead of schedule. Labor has pledged to match this. Given both sides have promised it, we think we can safely say it may not happen (are we being too cynical about politicians?)

- The Medicare levy will no longer go up from 2% to 2.5%. The Government announced that it would go up last year to fund the National Disability Insurance Scheme. We suppose this may well change again next year, who knows.

- There will be a new “tax speed limit” imposed of total tax take to GDP of 23.9%. These sorts of supposed hard and fast rules can be a bit silly in our opinion. We liken it to the legislated debt ceiling in the USA which they argue black and blue over every year and threaten to shut down the Government before they all agree to raise it and just move on. We suspect the “tax speed limit” problem will quickly go the same way as the “debt and deficit disaster” which no one ever talks about any more.

Bracket creep

The Government will lift some of the tax brackets which means taxpayers on those brackets will pay a bit less tax.

- The $87,000 threshold will be lifted to $90,000 from 1 July 2018

- In 2022/23 (that is a long way off!) the $37,000 threshold will be lifted to $41,000 and and the $90,000 threshold will be raised again to $120,000 (if they are still in Government and if they still want to do it)

- In 2024/25 (ie in the never/never) the Government plans to abolish the 37% bracket altogether (this is the bracket that currently ranges from $87,000 to $180,000). That means someone earning $38,000 will pay the same tax rate as someone earning $179,000 which is a massive change to how we tax income. This is not likely to ever be implemented as much will happen between now and then, even if the current Government does win the next two elections and finds itself in a position to do it.

- To put 2024 in perspective, that is the year the mother dies in the TV series “How I Met Your Mother” and the year the diaries of the Right Honourable James Hacker from Yes, Prime Minister are published. It’s also the year in Doctor Who when World War IV occurs (yes, I’m also wondering when WWIII occurred). We classify the 2024/25 planned Budget changes in the same fiction genre as each of these.

Both the Coalition and Labour have also promised to pay off Australia’s debt. It’s great to get clarity on that (we are being completely facetious here).

In addition, A Low and Middle Income Tax Offset (LITO AND MITO?) will now be available for individuals with incomes of up to $125,333.

Why ‘middle incomes’ need a tax offset is beyond us, we’d prefer if they just lowered the tax rate rather than the added complexity of taking your money with one hand and giving your money back with the other.

Good behaviour for SMSFs

Interestingly, the Government is going to reduce the audit requirements for SMSFs with a good history of

compliance from an annual audit each year to an audit every three years.

This will commence from 1 July 2019 and will apply to SMSFs that have:

- A history of 3 consecutive years of clear audit reports and

- Lodged the fund’s annual returns in a timely manner

This move should reduce costs for your SMSF (eg could reduce audit costs by 2/3rds). However, we make a caveat that the annual audit fee may go up if there is more work involved if it is audited less frequently. It will be interesting to see how this develops.

Who can be in your SMSF?

As flagged in the media prior to Budget night, SMSF will now be allowed to admit 6 members instead of four. As we wrote in the Australian Financial Review recently, “In my opinion, unless you have compelling reasons to include your children, more is not necessarily better for your SMSF.”

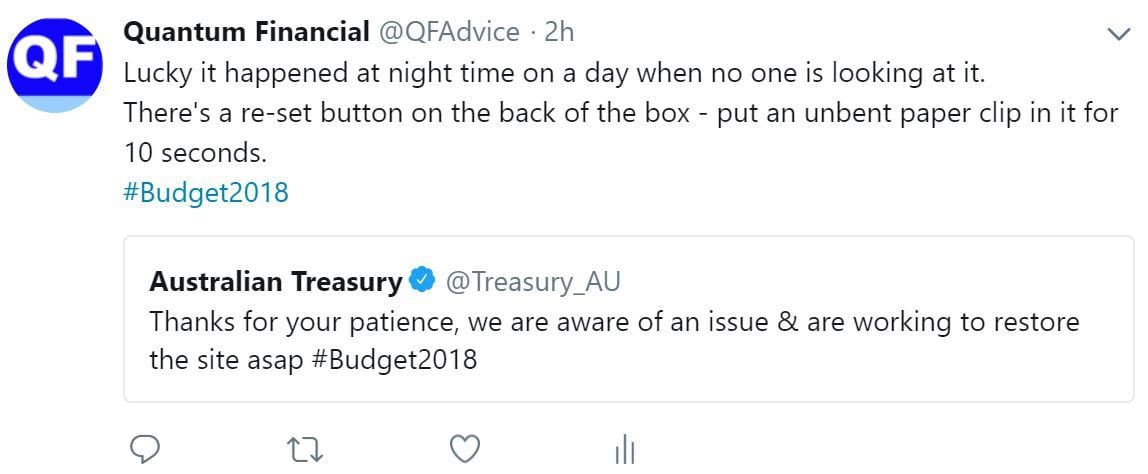

You can read our article titled “Who to include in your self-managed super fund” Another small but positive tweak to super is that exit fees when you leave your super fund will be banned. This is to be applauded. The current works test means you cannot personally contribute to your super once you reach age 65 unless you meet the work test (which is working for 40 hours over a 30 consecutive day period). The Budget tweaked this so that as long as your super member balance (combined across all your super funds if you have more than 1) is less than $300,000, then for those aged 65 to 74 you can skip the works test for one year only (it has to be the first year you don’t meet the work test). It’s a very small and quite complicated tweak but it could benefit some people, enabling them to contribute up to $100,000 personally in that year where they might otherwise not have been able. For those aged under 25 with a super balance less than $6,000, the Government is changing the super rules so that they have to opt-in to having life insurance. This replaces the current situation where they can be automatically enrolled in life insurance they typically don’t need and the fees just erode their already low super balances. This change won’t impact nay of our clients but it may impact your children or grand-children. We applaud the change but think it should apply to any super balance for young people, not just for those with less than $6,000 in their super. And while we’re at it, it should apply to anyone under age 120. In our opinion, all people should have the choice to opt-in to life insurance in super. It shouldn’t be forced upon them. The Pension Work Bonus will allow pensioners to earn an extra $1,300 a year without reducing their pension payments. Amendments to the pension means test rules may encourage some to invest in lifetime retirement income products. We are skeptical about the benefits of this. The Pension Loans Scheme will be opened to full rate pensioners and self-funded retirees. They can supplement their retirement income by up to $17,800 for a couple, without impacting on their eligibility for the pension or other benefits. This may allow more Australians to use the equity in their homes to increase their incomes. The Treasurer reiterated that “the Australian Financial Complaints Authority will stand up on 1 November”. We are proud that Treasurer Morrison’s colleague, Minister for Financial Services, Kelly O’Dwyer, recently appointed Claire Mackay to the Board of AFCA. You can read more [here]. This was our favourite 2018 Budget promise: “In addition to better weather and GPS services, there will be additional funding to protect against pests, disease and weeds.” We fully support the Government’s pledge of better weather. This is a great aspiration for any Government to make (yes, we know we are playing with words but it did makes us take a good hard second look at what he said hen we were analysing the Government’s commitments). Interesting, it seems Treasury uses the same crack team of IT experts that the Australian Bureau of Statistics (ABS) uses. So while the ABS’ site crashed on census eve, the Treasury’s website with all the Budget papers crashed on Budget evening; perhaps the only time people EVER look at the Treasury’s website. At the time, we offered Treasury our sage advice on how to resolve their problem. We will be completely honest here – this was not the most exciting Budget we’ve ever watched. It doesn’t hurt many groups and is more of a steady as she goes Budget; let’s hope the global pick up keeps going so tax revenues stay high. There were no negative changes to super or retirement planning, which is a relief after the negative changes in recent years. We completely understand if avoiding the Budget was your preference. The Voice, House Rules, MasterChef, a good book or even watching some quality paint dry may have been the more pleasant option. But we watched it because we need to know ANY changes that may impact the quality of advice that we give you. Even though we are finance tragics and look forward to Budget night every year, even we come to a point where the analysis and the journalists interviewing journalists to get a journalist’s perspective on the Budget gets too much. That’s when it’s time to go to bed. Even for us, the Budget excitement is well and truly over. Well, until next year. That’s all folks. Once again, dear reader, we commend our analysis of this Budget to the House.

Work test tweak

Life insurance opt-in

Changes for older Australians

Australian Financial Complaints Authority (AFCA)

Our favourite Budget promise

When you get to the end, stop

Leave A Comment